Elevate: Pricing, Packages

& Commercial Logic

Internal leadership document · 17 July 2026 · Prepared for review with Stewart · All figures in GBP; US-sourced benchmarks converted at £1 = $1.30 (planning FX from the group blueprint) · Sources in Section 17

Contents

- Executive summary

- What Elevate is: the hybrid model (and why the market is moving now)

- How this fits Stewart's 2026–2028 plan

- The engagement model

- The price card

- Package deep-dives

- Deliverables comparison matrix

- Bolt-on catalogue

- Price justification: the seven-angle case

- Pricing psychology: why the card is shaped this way

- Turnkey at scale: the pod model

- Revenue share logic

- What live delivery has taught us

- Contract standards and commercial governance

- How the model funds the company

- Decisions required

- References Appendix A. Complete deliverable inventory (register v2)

1. Executive summary

Elevate is not a D2C toolkit. It is the hybrid community-commerce model for direct selling organisations: the client keeps its network of sellers, and Elevate re-platforms that network onto branded consumer-grade infrastructure (storefronts, missions, real-time wallets, royalties across 10+ tiers, every payout tied to real sales) while adding the modern D2C engine (funnels, subscriptions, email/SMS, CRO, creators) that field-led businesses never built because the field was their channel. In the words of the public positioning: "Evolve the model. Keep the network."

Three packages priced on a gradient:

Platform £10–15K/mo · Managed Growth £22–31K/mo · Turnkey £46–65K/mo

plus a Strategy entry (£12.5–20K, 50% credited on proceed), a scoped Setup (£30–90K; native apps and field migration push toward the top band), a 4.5% revenue share on new business, and networks beyond ~10K active sellers scoped as dedicated instances from £20K platform.

The pricing case is built from seven independent angles (Section 9): the client's current spend on legacy MLM software (enterprise platforms run £23K+/month for software alone), the risk value of a compliant transition in a market where peers are collapsing, economic value to the customer, the assemble-it-yourself market composite, the in-house build cost, channel take-rate economics, and LUUP's own delivery cost floor. No single comparison carries the argument; all seven converge on the same card.

2. What Elevate is: the hybrid model (and why the market is moving now)

The model. Direct selling organisations grow through people. Elevate does not ask them to abandon that; it gives the network consumer-grade tools under the client's own brand: a branded seller app (native iOS/Android or web) with storefronts, missions, sharing tools and real-time wallets; a royalty architecture across ten tiers or more in which every payout traces to a real customer sale; and, around the network, the full D2C engine (personalised funnels, subscriptions, membership, lifecycle automation, creator commerce) that turns the client from field-only into hybrid: field + creators + direct customers on one platform, one attribution spine, one payout rail.

Why now: the regulatory clock. The public site states it plainly: "Markets and regulators increasingly expect rewards that trace to real sales." The evidence behind that sentence:

- The FTC's September 2024 staff report analysed income disclosures from 70 MLMs: most participants made $1,000 or less per year, and in at least 17 companies most participants made nothing.

- Beachbody/BODi shut down its MLM network on 1 January 2025 and replaced it with an affiliate programme.

- Rodan + Fields moved from consultant MLM to a single-level affiliate model in September 2024, removing downline commissions entirely.

- Tupperware entered bankruptcy; wellness MLM Modere closed in April 2025 citing regulatory and financial pressures.

Every direct selling board is now choosing between three doors: transition badly alone (Rodan + Fields cut jobs and field income overnight; the companies above lost their networks or their existence), do nothing (Tupperware, Modere), or transition onto infrastructure built for exactly this move. Elevate is the third door, and its migration methodology answers the board's biggest fear: seller records, network structure and earnings ledgers arrive whole; payouts never skip a cycle (parallel running until the numbers reconcile); rollout is staged by market or team with training. The platform's reporting is structured to support disclosure and regulatory requirements per market.

Why this reframe matters for pricing: the buyer's reference costs are direct-selling costs, not D2C costs. Their current stack is enterprise MLM software plus field-enablement tools, both priced far above DTC SaaS. Their downside scenario is not "a campaign underperforms"; it is the model itself becoming unsellable. Both push willingness-to-pay well above D2C benchmarks, and Section 9 prices against that reality.

3. How this fits Stewart's 2026–2028 plan

The group Frame is $100M (~£77M) monthly net attributed GMV by July 2028, Elevate carrying $80M via ten contracted enterprise clients (December 2026), sourced through ~50 executive discovery meetings → ~25 workshops → ~15 paid design partnerships → 10 contracts. Elevate's public credibility assets anchor the pipeline: infrastructure built by the team behind an affiliate network that tracked £1B+ in sales, with the founder's story front and centre.

Pricing is the bridge between that plan and a bootstrapped present. Its four jobs:

- Fund the company now. At target scale, transaction revenue outweighs service fees roughly 12-to-1; for the next 12–18 months the ratio is reversed. Service fees are the survival mechanism: every package must be cash-positive standalone, from signature.

- Enable the funnel. A £400M+ direct seller must be able to say yes in stages: a Strategy commitment signable on discretionary authority, a bounded Setup, a monthly operation, a revenue share that bites only as the new channel succeeds.

- Protect the take-rate ambition (group guardrail: 4%+ blended). The one deliberate deviation is isolated as a leadership decision in Section 12.

- Prevent the named failure mode: "Turnkey delivery begins to resemble unbounded Bespoke work" (group risk register). Answered structurally by allowances, priced bolt-ons, and the pod capacity model in Section 11.

4. The engagement model

Aligned with the five phases on the public site (Scope → Design → Build → Launch → Run):

| Phase | What happens | One-time / Ongoing | Commercial |

|---|---|---|---|

| 1. Scope & Design (Elevate Blueprint) | Model audit, market and regulatory scan, royalty architecture, community journeys, D2C funnel and offer design, app experience, integration map, rollout plan | One-time | £12.5–20K by scope, fixed · 50% credited against Setup on proceed within 60 days |

| 2. Build | Branding, website & funnel build, app build (native or web), royalty and payout configuration, integrations, data migration, flows, first missions, testing | One-time | £30–90K scoped · 50% signature / 50% UAT |

| 3. Launch | Staged rollout by market/team, field training, guided activation | One-time | Included in Setup |

| 4. Run | Platform / Managed Growth / Turnkey | Ongoing | Monthly in advance, from signature |

| 5. Scale | Markets, brands, programme expansion | Ongoing | Bolt-ons + multi-country framework |

Why the Blueprint leads and why it's priced at £12.5–20K: strategy at this depth is billed by fractional CMOs at £9–17K per month and transformation consultancies at multiples of that; for a direct seller it also carries the royalty-architecture modelling the site promises ("modelled with your team during design"). £12.5–20K is real money that kills the free-consulting failure mode, yet sits inside a sponsoring executive's discretionary signing authority: no procurement cycle for the first yes. The 50% credit against Setup (on proceed within 60 days) removes the "paying twice for scoping" objection while respecting that the Blueprint has standalone value. On the group funnel (15 paid design partnerships), this phase contributes ~£190–300K of 2026 cash from the pipeline.

5. The price card

The public site says "scoped to your requirements, not a tier list", and this card honours that: externally, every engagement is scoped and quoted individually with "from" prices; internally, every scope maps to exactly one band below. The bands are the scoping discipline that makes "custom" profitable. Clients negotiate scope, never price.

| Package | Range | Driver 1: markets | Driver 2: programme volume | Driver 3: network scale |

|---|---|---|---|---|

| Platform | £10K floor → £15K | 1 market at floor; +£1.5K per market | Base allowances | ≤2,500 active sellers at floor |

| Managed Growth | £22K → £31K | 1 market at floor | 8 campaigns / 6 journeys / 4 experiments at floor | Bands below |

| Turnkey | £46K → £65K | 1 market at floor | 12 campaigns / 12 assets / 25 creators at floor | Bands below |

The Platform floor is exactly the current live contract price (£5K licence + £5K platform-services): no repricing risk on the existing base. Networks beyond ~10K active sellers are scoped as dedicated Elevate instances, platform from £20K/month, reflecting dedicated infrastructure, payout volume and support load.

Banding (internal price book):

| Band | Managed Growth | Turnkey | What moves a client up |

|---|---|---|---|

| Band 1 (floor) | £22K | £46K | Single market, base allowances |

| Band 2 | £26K | £55K | Second market, or ~1.5× allowances, or complex integrations in operation |

| Band 3 (ceiling) | £31K | £65K | Multi-market single instance, high programme volume, weekly executive reporting |

| One-time / variable | Amount |

|---|---|

| Strategy (Elevate Blueprint) | £12.5–20K fixed by scope |

| Setup & build | £30–90K scoped: ~£30–45K standard web build · ~£45–70K complex integrations or native apps · ~£70–90K enterprise migration with parallel payout runs |

| Revenue share (new business) | 4.5% of net tracked sales, monthly in arrears |

| Revenue share (existing/migrated business) | 0% standard; 0.5% option (Section 12) |

| Payout processing | 2.5% of payouts |

| Transaction minimum (non-flagship deals) | £6K/month from month 4 post-launch, fully credited against actual revenue share |

| Annual prepay | 8% discount, offered as a client option only |

6. Package deep-dives

6.1 Platform: from £10K/mo · "We run your network's infrastructure"

For: organisations with a real internal marketing and field operations team. Qualifying question: who, by name, operates missions, funnels, flows and field activation? No confident answer → wrong tier (Section 13).

Scope: the complete network and commerce infrastructure: white-label branded platform (web + PWA; native apps where built), the commerce website built in Setup (hosted, maintained, supported to SLA), royalty architecture with 10+ tiers calculated automatically and tied to real sales, real-time wallets and payout schedules with float management, KYC and payout tax documentation, fraud and attribution-integrity monitoring, tracking and attribution across web/app/checkout, storefronts, missions infrastructure, compliance and disclosure-ready reporting, segmentation, multi-language/currency as configured, analytics and monthly reporting. The client operates everything; we keep it running, accurate and audit-ready.

Why the £10K floor is non-negotiable: it is the current live price point, and the client's own reference class defends it independently. Enterprise MLM platforms run to custom pricing exceeding $30K (~£23K) per month for software alone, before field-enablement tools (Rallyware/Penny-class, priced per distributor), commerce, email or creator software. Even in the D2C world, creator SaaS runs £21–77K+/year and impact.com charges 2.5% of partner-driven sales on top of SaaS fees. Platform bundles the network engine, the commerce site, white-label apps and payout rails. Below £10K a client cannot generate Elevate-relevant GMV and belongs in LUUP One (£695/mo self-serve).

6.2 Managed Growth: from £22K/mo · "We operate your growth programmes" (recommended default)

Everything in Platform, plus LUUP operates both sides of the hybrid engine:

- Network activation: mission and campaign creation, activation and optimisation (8/mo at floor); seller recruitment and onboarding journeys; storefront optimisation; referral, loyalty, Friends & Family and membership programme operation. Clear weekly actions for every seller: share, post, refer, host.

- Website & funnel operations: landing pages, advertorials and campaign funnels from the template library; offer, bundle and upsell/cross-sell configuration; promotions calendar; quiz and product-finder iteration; merchandising; popups, exit-intent and cart-recovery experiences.

- CRO programme: experiment pipeline (4/mo at floor) across landing pages, PDPs, cart and checkout; funnel analytics; personalisation by source, segment and behaviour.

- Email/SMS & CRM: the full lifecycle flow suite operated on the client's tooling: welcome, browse and cart abandonment, post-purchase, replenishment, win-back; campaign sends and newsletters; segmentation and zero-party data capture; subscription dunning and failed-payment recovery; deliverability management.

- Reporting: monthly performance review; campaign calendar; recommendations.

Team behind it (floor band): campaign/mission operator (~0.75 FTE), lifecycle/email specialist (~0.4), growth lead (~0.2), designer (~0.25), analyst (~0.15), plus platform support.

6.3 Turnkey: from £46K/mo · "We own your growth engine"

Everything in Managed Growth at raised allowances (12 campaigns, 6 experiments, 10 flows), plus the layers that make it the full managed service the site describes under "Run":

- Content & demand engine: creative strategy; production of education, offer and campaign assets (12/mo at floor); ad creative variants; seasonal campaigns; mission planning and creative direction.

- Creator & seller programme (managed service): sourcing, outreach, negotiation, gifting logistics, briefs and performance management for up to 25 active creators at floor, alongside field-leader activation programmes. Human-powered Scout; automation arrives as margin improvement, not a re-sale.

- Social proof operations: capture is nearly free at every tier because the missions engine does it (a structural cost advantage over agencies, who bill retainers for what our platform automates). Turnkey adds everything after capture: rights, consent and usage-expiry management; curation and deployment across funnels, PDPs, storefronts, email and checkout; review and testimonial programmes; A/B testing of proof placement; the winning-content loop into ads and campaigns.

- Retention economics: subscription and membership architecture management, welcome kits, save offers, churn and cohort analysis across customers and sellers.

- Ownership layer: dedicated growth lead (~3 days/week), weekly dashboards, monthly business review, quarterly growth roadmap. One owner, one report, one accountable number.

Team behind it (floor band): growth lead (~0.6 FTE), campaign/mission operator (1.0), lifecycle specialist (~0.75), content producer (1.0), creator/field ops manager (1.0), designer (~0.5), analyst (~0.4), plus platform support. Roughly 6 FTE of specialist capacity, which is why Turnkey is capacity-managed (Section 11).

7. Deliverables comparison matrix

The operating view: what each package does month to month. (The exhaustive inventory, including everything delivered in Scope/Design and Build, is Appendix A.)

Legend: ● included · ◐ included to allowance (more = bolt-on) · ○ bolt-on · CR client-run on our infrastructure · n/a not at this tier

| # | Ongoing deliverable | Platform | Managed Growth | Turnkey |

|---|---|---|---|---|

| NETWORK, ROYALTY & FIELD OPERATIONS | ||||

| 1 | Royalty architecture (10+ tiers, tied to real sales), automatic calculation | ● | ● | ● |

| 2 | Real-time wallets, payout schedules & float management | ● | ● | ● |

| 3 | Payout processing (2.5%), KYC & payout tax documentation | ● | ● | ● |

| 4 | Royalty/comp-plan change modelling & deployment | ◐ 1/qtr | ◐ | ◐ |

| 5 | Disclosure & regulatory reporting data structure | ● | ● | ● |

| 6 | Seller recruitment & onboarding journey operation | CR | ● | ● |

| 7 | Field training & enablement (post-launch) | ○ | ◐ | ● |

| 8 | Fraud, chargeback & attribution-integrity monitoring | ● | ● | ● |

| CORE PLATFORM & INFRASTRUCTURE | ||||

| 9 | White-label branded platform (web + PWA; native apps where built) | ● | ● | ● |

| 10 | Website hosting, maintenance & technical support | ● | ● | ● |

| 11 | Tracking & attribution across web, app & checkout | ● | ● | ● |

| 12 | Personal links, codes & seller/creator storefronts | ● | ● | ● |

| 13 | Missions & campaign infrastructure | ● | ● | ● |

| 14 | Content approval & compliance controls | ● | ● | ● |

| 15 | Cookie consent & data-protection operations (GDPR/DPA) | ● | ● | ● |

| 16 | Segmentation (customer/member/seller/creator) | ● | ● | ● |

| 17 | Multi-language & multi-currency (as configured) | ● | ● | ● |

| 18 | Analytics, dashboards & monthly reporting | ● | ● | ● |

| 19 | SLA support (4-business-hour critical response; 99.5% uptime target) | ● | ● | ● |

| WEBSITE & COMMERCE OPERATIONS | ||||

| 20 | Site content updates & merchandising | ○ | ● | ● |

| 21 | Landing pages, advertorials & campaign funnels (new) | ○ | ◐ | ◐ |

| 22 | Source-specific pages (sellers, creators, podcasts, partners, paid) | ○ | ◐ | ◐ |

| 23 | Offer, bundle & pricing configuration | CR | ● | ● |

| 24 | Upsell / cross-sell / free-gift mechanics | CR | ● | ● |

| 25 | Popups, exit-intent & cart-recovery experiences | CR | ● | ● |

| 26 | Cart & checkout optimisation | n/a | ● | ● |

| 27 | Product-finder quiz operation & iteration | CR | ● | ● |

| 28 | Promotions & offers calendar | CR | ● | ● |

| 29 | Subscription programme management (plans, dunning, saves) | CR | ● | ● |

| 30 | Membership / Club & Friends & Family programme operations | CR | ● | ● |

| CRO & EXPERIMENTATION | ||||

| 31 | A/B testing programme | n/a | ◐ 4/mo | ◐ 6/mo |

| 32 | Funnel analytics & conversion reporting | ● (reports) | ● (operated) | ● (operated) |

| 33 | Personalisation by source, segment & behaviour | n/a | ● | ● |

| CRM, EMAIL & SMS | ||||

| 34 | Lifecycle flows: welcome, browse & cart abandonment, post-purchase, replenishment | CR | ◐ 6 maintained | ◐ 10 maintained |

| 35 | Win-back & reactivation campaigns (customers & sellers) | CR | ● | ● |

| 36 | Campaign sends & newsletters | CR | ◐ 4/mo | ◐ 8/mo |

| 37 | Segmentation & zero-party data programmes | CR | ● | ● |

| 38 | SMS programmes | ○ | ◐ | ● |

| 39 | CRM management & sales-feed integration | ○ | ● | ● |

| 40 | Email/SMS deliverability management (domains, warmup, hygiene) | ○ | ● | ● |

| ADVOCACY & PROGRAMME OPERATIONS | ||||

| 41 | Mission & campaign creation, activation, optimisation | CR | ◐ 8/mo | ◐ 12/mo |

| 42 | Referral & loyalty programme activation | CR | ● | ● |

| 43 | Storefront optimisation | n/a | ● | ● |

| CONTENT & CREATOR ENGINE | ||||

| 44 | Content production (education, offers, campaign creative) | n/a | ○ | ◐ 12 assets/mo |

| 45 | Ad creative variants for paid channels | n/a | ○ | ◐ |

| 46 | Creator sourcing, outreach, gifting & management | n/a | ○ | ◐ 25 creators |

| 47 | Social proof capture via missions (reviews, testimonials, UGC) | CR | ● (within mission allowance) | ● |

| 48 | UGC rights, consent & usage management (reuse in owned/paid channels) | n/a | ○ | ● |

| 49 | Proof curation, deployment & testing (site, email, checkout, ads) | n/a | ○ | ● |

| 50 | Giveaways, sampling & event activations | ○ | ○ | ◐ |

| 51 | Paid media management | ○ | ○ | ○ |

| 52 | SEO programme | ○ | ○ | ○ |

| REPORTING & GOVERNANCE | ||||

| 53 | Monthly performance review | ○ | ● | ● |

| 54 | Weekly dashboards | n/a | ○ | ● |

| 55 | Monthly business review (MBR) | n/a | ○ | ● |

| 56 | Churn, cohort & retention analysis (customers & sellers) | n/a | ○ | ● |

| 57 | Quarterly growth roadmap | n/a | n/a | ● |

| 58 | Dedicated growth lead | n/a | n/a | ● |

| SCALE (bolt-on at any tier) | ||||

| 59 | Additional markets / languages | ○ | ○ | ○ |

| 60 | Additional brand instances | ○ | ○ | ○ |

| 61 | Custom integrations (ERP/CRM/other); headless deployment | ○ | ○ | ○ |

| 62 | Data & field migration (post-launch phases) | ○ | ○ | ○ |

| 63 | Third-party licences (email/SMS, reviews, quiz, subscription tools) | pass-through | pass-through | pass-through |

The boundary rule: infrastructure is included; operation is tiered; volume is bolted on. Anything whose cost scales with the client's success can never sit inside a flat fee.

8. Bolt-on catalogue

| Bolt-on | Price | Basis |

|---|---|---|

| Additional market/language | £4.5K/mo per market | Localisation, ops & reporting load |

| Additional brand instance | £3K/mo per brand | Configuration & management |

| Mission/campaign pack (+4/mo) | £2.5K/mo | ~0.5 operator-week |

| Lifecycle journey build | £2.5K one-time per journey | 3–4 days build |

| Email/SMS campaign pack (+4/mo) | £2K/mo | Specialist time |

| Content pack (+8 assets/mo) | £4K/mo | ~1 producer-week |

| Creator band (+25 creators) | £4K/mo | ~1 coordinator-week; agencies price 10–20 creators at ~£12K/mo |

| CRO expansion (+2 experiments/mo) | £2K/mo | Analyst + operator |

| Royalty/comp-plan restructure (beyond quarterly allowance) | Scoped from £7.5K | Modelling + configuration + parallel verification |

| Field training programme (new market/team) | £1.5K per session block | Trainer time |

| Paid media management | 10% of spend, £4.5K/mo min | Industry standard 10–20% of spend; spend stays client-side |

| SEO programme | £3–6K/mo scoped | Market rate for retained SEO |

| Giveaway / sampling / event activation | Scoped from £6K per activation | Production + ops |

| Product photography & brand asset production | Scoped per shoot | Third-party + coordination |

| Community / social channel management | £3–5K/mo scoped | Specialist time |

| Reporting upgrade (weekly + MBR on lower tiers) | £1.5K/mo | Analyst day/mo |

| Custom integrations / headless | Scoped from £12K + 15%/yr maintenance | Complexity-driven |

| Data/field migration (post-launch phases) | Scoped from £15K | Complexity-driven |

| High-risk payment processor sourcing & setup | Scoped from £5K | Specialist sourcing (live-contract precedent) |

| Native app build (where not in original Setup) | Scoped from £25K | iOS + Android build & store management |

| Third-party licences | Cost + 12% handling | Never absorbed |

Excluded from everything, deliberately: paid media spend (client budget, always); legal opinions on compensation structures (we provide the data structure and coordinate; the client's counsel owns the opinion); anything "unlimited"; Scout-as-software until it ships.

9. Price justification: the seven-angle case

A pricing expert never rests a price on one comparison. Seven angles, each independent; the card must survive all of them. (US-sourced figures converted at £1 = $1.30.)

Angle 1: Reference-price analysis — what this buyer already pays

Willingness-to-pay starts from what the buyer's category already spends, and direct selling technology is expensive:

- Enterprise MLM platforms (Exigo, DirectScale class) are custom-priced, with enterprise-level packages exceeding $30K (~£23K) per month for the commission engine, back office and shopping platform alone.

- Field-enablement suites (Rallyware, Penny-class) are priced per distributor on top; at field sizes in the tens of thousands these run to six figures annually.

- Implementation and comp-plan configuration for legacy platforms is a separate six-figure exercise, and changes are slow: the public site's comparison line, "hard-coded, slow to change", is the lived experience of this buyer.

A £400M+ direct seller typically carries £30–80K+/month of network software cost across this stack, before any marketing capability exists at all. Elevate's Platform (£10–15K, or from £20K as a dedicated instance) replaces the commission engine, back office, field app and payout tooling and adds the commerce site; Managed Growth and Turnkey add the operating capability the legacy stack never had. Against the buyer's own reference class, the card reads as consolidation and a saving, not a new cost.

Angle 2: Risk value — what a failed or absent transition costs

For this buyer, pricing is measured against downside, not just upside:

- Do nothing: Tupperware is in bankruptcy; Modere closed in April 2025; the FTC's 2024 report signals where enforcement is heading.

- Transition alone, badly: Rodan + Fields' overnight shift cut downline income with no replacement engine; field revolt and revenue collapse are the standard outcomes, with 10–25% of revenue typically lost during self-managed ramps.

- Transition on Elevate: earnings ledgers migrate whole, payouts never skip a cycle (parallel runs until reconciliation), rollout staged with training, and rewards demonstrably trace to real sales from day one, with disclosure-ready reporting.

For a company doing £400M annually, 10% revenue protection is £40M. Against that, the entire first-year Turnkey cost (~£620–850K including Setup) is under 2.2% of the protected amount. Risk-transfer value alone supports the card several times over; this is the argument that belongs in the boardroom.

Angle 3: Economic value to the customer (EVC)

EVC = the client's next-best alternative cost + the differentiated value Elevate adds. Next-best alternative: keep paying the legacy stack (Angle 1: £30–80K/mo) and hire an in-house D2C team (Angle 5: £35–100K/mo) and accept self-managed transition risk (Angle 2). Elevate's differentiated value: one platform replacing both stacks, a proven migration method, and a new-business engine (creators + funnels + subscriptions) the client has never operated. Formally, EVC for a mid-size transition sits at £65–180K/month; Turnkey's £46–65K captures roughly a third to a half of the value created, which is textbook value-pricing discipline (the customer keeps most of the surplus, so the deal stays easy to say yes to).

Angle 4: The assemble-it-yourself market composite

If the client sourced Elevate's scope from specialists: full-stack DTC growth agency £15–58K/mo + influencer agency £2.5–19K/mo plus 15–30% creator markups + tier-1 affiliate OPM £6–19K/mo plus 5–15% performance fees + CRO agency £8–23K/mo + email agency £2–6K/mo + site retainer £2–15K/mo ≈ £45–127K/month plus performance fees, across five or six vendors, none of which can run a royalty network, wallets or payouts. Managed Growth's scope alone composites to £15–47K/month across four vendors. The card sits at or below the composite midpoints as one accountable partner.

Angle 5: The in-house build cost

Whole heads, US big-city loaded rates (×1.35, converted): a Managed Growth-equivalent team (growth manager £11.2K + lifecycle £9.9K + fractional design/dev £7K + SaaS £3–9K + recruiting amortised £4K) ≈ £35–42K/month; a Turnkey-equivalent team (director £15.2K + growth £11.2K + lifecycle £9.9K + content £9.8K + creator ops £9.5K + designer £8.2K + developer £6–12K + analyst £5K + tools £5–9K + recruiting £10–13K) ≈ £85–100K/month in year one, with an 8+ month ramp before results, and still no royalty engine, wallets, or field migration capability, because those cannot be hired at any price short of building a software company. Salary sources: Salary.com, Glassdoor NYC, Glassdoor, recruiting cost basis.

Angle 6: Channel take-rate economics

The complete cost of the Elevate channel at maturity: a £1.5M/month GMV client on Turnkey Band 2 pays £55K fees + £67.5K revenue share = 8.2% total channel take. The comparisons every CFO knows: Amazon runs ~15% referral plus fulfilment and advertising (25–30% all-in); app stores take 15–30%; impact.com charges 2.5% of partner sales for software alone; agency-plus-network affiliate stacks run 10–20% with markups. Supporting checks: the fee passes the sub-15%-of-revenue-responsibility rule at every band (MG Band 1 needs ≥£147K/month of responsibility; targets are multiples of that), and payback at a 70% product margin arrives at £31K/month incremental GMV for MG Band 1.

Angle 7: Cost-plus floor and capacity pricing

LUUP's blended global delivery cost (≈50% of US-equivalent load): Platform ~£3.5K, Managed Growth ~£14K, Turnkey ~£31K per month → gross margins of 65–77% / 36–55% / 33–52% across the bands. Floors are the thinnest margins deliberately: floors win deals, bands and bolt-ons restore margin as scope grows. On top of cost-plus sits capacity pricing: Turnkey consumes ~6 FTE of specialist capacity and is throttled to two launches per quarter (Section 11); a supply-constrained flagship is priced to ration demand, or the queue destroys both margin and reputation.

Convergence. Angle 1 says the buyer already pays more for less. Angle 2 says the risk retired is worth multiples of the fee. Angle 3 says we capture under half the value we create. Angles 4 and 5 say every alternative costs more and delivers less. Angle 6 says the mature channel is the cheapest the client will operate. Angle 7 says every band is profitable to deliver. Seven angles, one card.

10. Pricing psychology: why the card is shaped this way

The card's structure applies documented pricing research, not taste:

- Anchoring. The first number a buyer sees becomes the reference for everything after. Proposals open with the legacy-stack spend (£30–80K/month), the in-house cost (£85–100K) and the risk arithmetic (Angle 2) before any Elevate price appears; Simon-Kucher's work puts effective anchoring at 15–20% higher average contract values. Our card is presented top-down, Turnkey first, for the same reason.

- The compromise effect. Buyers choosing among three options disproportionately select the middle one, documented by Simonson and refined across three decades of choice research. The card is engineered for it: Platform is the credible floor, Turnkey the premium anchor, and Managed Growth (the tier we most want to sell, and our best margin-to-capacity ratio) is the safe middle. Three to four tiers is the researched optimum.

- Meaningful gaps. The compromise effect weakens when tiers are priced too closely. The ladder steps at roughly 2.2× per tier (£10 → £22 → £46): each step reads as a different class of relationship, not a haggling opportunity.

- Precise numbers, not round estimates. Band prices (£22K, £26K, £55K) read as computed from cost and scope; round numbers read as opening bids and invite negotiation. Enterprise B2B punishes charm pricing; the card uses none.

- "Scoped, not tiered" as framing. The public site's promise ("scoped to your requirements, not a tier list") is itself sound psychology for this buyer: enterprise direct sellers expect bespoke treatment, and scoping preserves price integrity while flattering the buyer's uniqueness. The internal bands make bespoke profitable.

- Partitioned pricing. The two-line invoice (platform licence + growth services), already live-contract practice, keeps the infrastructure fee anchored while service scope flexes; procurement can cut scope without ever cutting price per unit of scope.

- Loss aversion in the close. The 50% Blueprint credit expires 60 days after delivery: proceeding "saves" money already spent. Deadline plus sunk investment is the strongest ethical close available.

- The decoy function of the ceilings. Platform's £15K ceiling sits close to MG's £22K floor by design: expansion pressure converts into upgrades.

11. Turnkey at scale: the pod model

Turnkey is the highest-effort product and the group's own risk register flags managed-service delivery overwhelming the team. The answer is structural:

The Growth Pod. One pod = growth lead + campaign/mission operator + lifecycle specialist + content producer + creator/field ops manager, with shared design and analytics. One pod serves exactly two Turnkey clients (or one Turnkey + two Managed Growth). Pod economics at Band-2 average: ~£110K/month revenue against ~£62K blended pod cost → ~44% pod-level margin before revenue share.

Capacity rules:

- Onboarding throttle: maximum two Turnkey launches per quarter. Demand beyond capacity starts on Blueprint + Managed Growth and upgrades on a scheduled slot; the waitlist is a sales asset, not an apology.

- Hiring trigger: a new pod is hired when contracted demand exceeds 80% of existing pod capacity. Signed contracts fund headcount, never forecasts (the group's "build after commitment" floor).

- Margin tripwire: any Turnkey client below 30% gross margin for two consecutive months triggers a scope/band review. Allowances are enforced by measurement, not goodwill.

- Productisation curve: every deliverable ships from the shared playbook library (missions, journeys, funnels, briefs); each repeat vertical targets 20–30% effort reduction. Scout automation progressively removes the largest manual bucket. Margin expansion comes from delivery leverage, not from repricing existing clients.

- Mix guardrail: no more than ~60% of active clients on Turnkey until three pods run at target margin simultaneously.

12. Revenue share logic

4.5% on new business. The precedent stack: impact.com charges 2.5% of partner-driven sales on top of SaaS, for software alone; performance agencies take 5–15% of revenue generated; tier-1 OPMs layer 5–15% performance fees on retainers; influencer agencies add 15–30% creator markups. At 4.5% on new business only, with the platform, royalty engine, payout rails and managed growth included, Elevate sits 2 points above a software company's transaction fee and far below every services benchmark.

Existing/migrated business: 0% standard, and the decision Stewart must own. In a hybrid transition, the migrated field volume is the client's lifeblood; not taxing it is the objection-killer that wins flagship deals. But the group model assumes 4.5% on all attributed GMV (~£33M of ~£44M recurring at scale, converted), and for a full model transition, most volume eventually flows through Elevate. If half of mature GMV is migrated at 0%, blended take falls to ~2.25% and the 4% guardrail breaks. Recovery levers (0.5% on migrated volume, worth ~£1.8M/year at scale; a year-two step-up; or the £6K minimums) must be chosen once, before the first flagship contract sets precedent for ten. The definition of "new business" (new customers? new channels? volume above a migrated baseline?) must be contractually exact; a baseline-and-growth definition is recommended.

2.5% payout processing: mass-payout providers charge ~2% before FX; priced near cost deliberately because payouts-through-platform is the adoption lever (Section 13).

13. What live delivery has taught us

Our longest-running live referral deployment (a B2B client, ~1,500-customer base, structured reward-per-referral programme) carries three load-bearing lessons:

Adoption is a service, not a feature. Despite meaningful rewards, only a small percentage of the base ever referred through the platform; most bypassed the app and emailed leads directly to sales reps, because the old habit was frictionless and nobody operated the new one. For a direct-selling field with decades of ingrained habits, this risk is many times larger. It is why Managed Growth is the default recommendation, why Platform-only requires named internal operators, and why field training and staged rollout are core Setup deliverables.

The payment rail is the adoption lever. The identified fix: make the platform the only mechanism through which rewards are paid. In a royalty network this is structural: sellers live where their wallet lives. It drives adoption, protects attribution, and underpins the 2.5% fee.

Payment discipline cannot be optional. The same client consistently pays a month or more late, consuming team time in collections. That lived experience is why advance billing, deposits before work and standing-order collection are contract standards, not preferences. A bootstrapped company cannot fund enterprise clients' working capital.

14. Contract standards and commercial governance

- Monthly fees from signature, or a reduced onboarding rate during build with a hard week-13 backstop. Never gated on a launch date the client controls.

- Everything recurring billed monthly in advance; setup deposits before work; standing order / direct debit as default collection.

- Formal change control; no verbal approvals. Royalty/comp-plan changes beyond the quarterly allowance are scoped work.

- Allowances and band definitions written into schedules; band moves are pre-priced, never renegotiated.

- 12-month initial term, auto-renew; annual prepay at 8% as a client option.

- Discount governance: the only standard discount is the prepay 8%. Any other concession requires Stewart's written approval, and must be traded for something: term length, case-study rights, volume commitments, or an expanded rev-share base.

- Indexation: fees rise annually at CPI + 2% unless renegotiated; written into every contract.

- Currency: pricing denominated in GBP; USD or EUR invoicing available at a quarterly-fixed rate.

- Exclusivity only by separately signed addendum (territory, category, duration, limits).

- Compliance boundary in every contract: Elevate provides the data structure, tracking and disclosure-ready reporting; the client's counsel owns compensation-plan legality in each market. Never sold otherwise.

- Hygiene: one governing law throughout (the current template carries a contradiction to fix); every included service listed explicitly in schedules.

15. How the model funds the company

Service MRR only, before Blueprint fees, Setup, bolt-ons, revenue share, and the existing client base (band midpoints):

| Milestone | Illustrative mix | MRR |

|---|---|---|

| First proof | 2 × Managed Growth (Band 1–2) | ~£48K |

| End-2026 minimum (3 live) | 2 × MG + 1 × Turnkey | ~£103K |

| End-2026 contracted (10) | 2 × Platform + 5 × MG + 3 × Turnkey | ~£320K |

| Group base case | 2 × Platform + 8 × Turnkey | ~£465K |

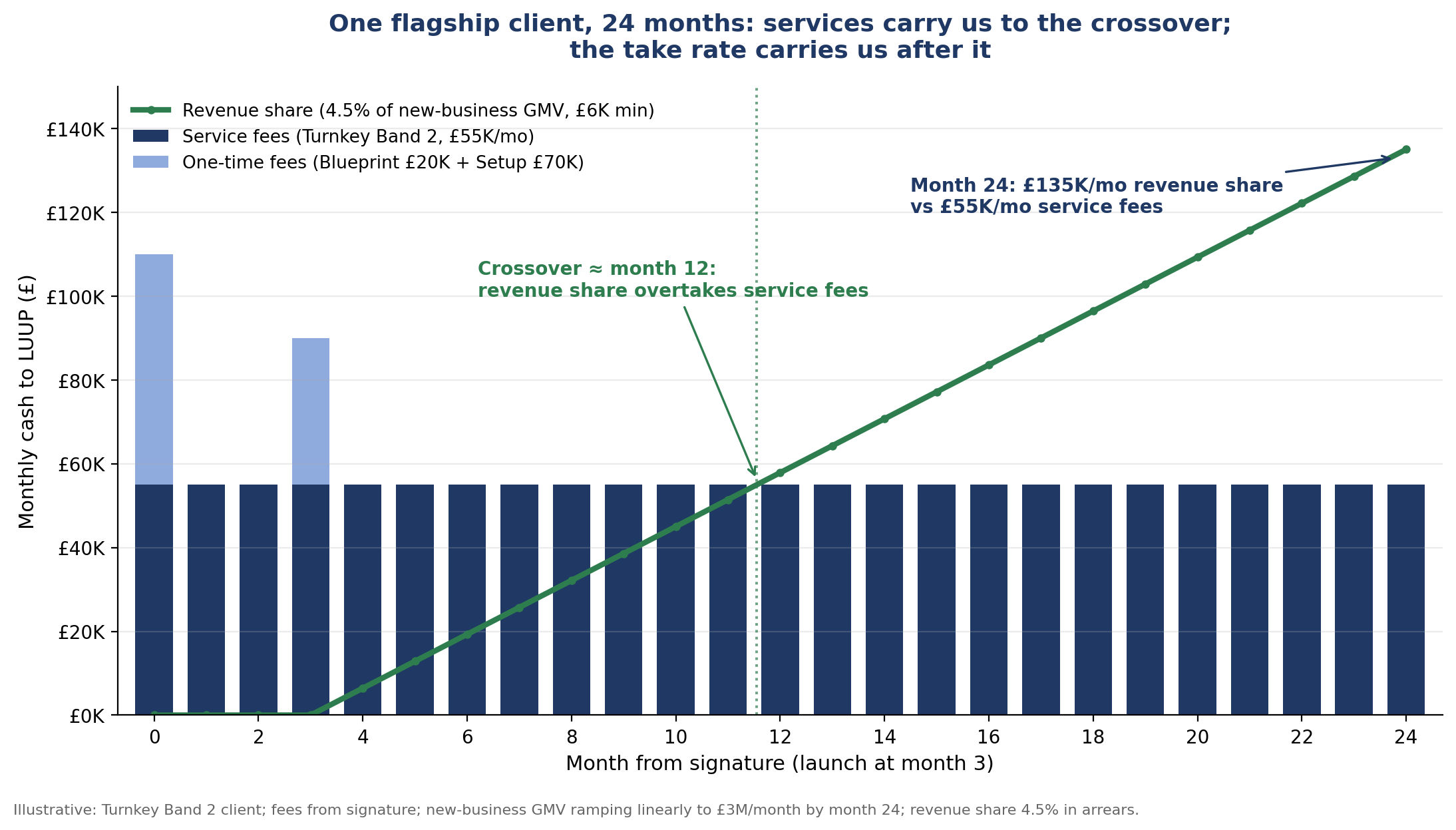

A single Managed Growth client at Band 1 materially closes the current funding gap; two end founder support. Each enterprise signing delivers £95–260K of cash in its first 90 days (Blueprint fee + Setup deposit + three advance-billed months). Then the second engine matures: one client generating £3M/month of new business pays £135K/month in revenue share, more than a full pod's service revenue. Services carry us to the crossover; the take rate carries us after it.

The crossover, visualised

One flagship client, 24 months from signature. Service fees (£55K/month, Turnkey Band 2, billed from signature) plus one-time fees (£20K Blueprint, £70K Setup) carry the engagement through build and early ramp. Revenue share at 4.5% of new-business GMV (£6K monthly minimum from month 4) overtakes service fees at roughly month 12, and reaches ~£135K/month by month 24 on a £3M/month new-business ramp. The same crossover repeats for every client in the portfolio, which is the entire commercial story in one picture: the fees fund the company while the take rate matures; the take rate then dwarfs the fees. Assumptions are deliberately conservative: a linear ramp, a single market, and no bolt-ons, band moves or existing-business share.

16. Decisions required

- Approve the gradient price card (Section 5): floors, ceilings, band drivers, the dedicated-instance threshold, and the £6K transaction minimum.

- Approve the Turnkey capacity rules (Section 11): throttle, hiring trigger, margin tripwire, mix guardrail.

- Decide the existing/migrated-business revenue share position and the contractual definition of "new business" (Section 12), once, before the first flagship contract.

- Approve the commercial governance set (Section 14), including the compliance boundary clause.

- Ratify the blended delivery-cost assumption (~50% of US-equivalent) against actual payroll; Angle 7 margins recalculate from it.

- Approve the multi-country renegotiation framework before a flagship asks for it.

17. References

Positioning: Luup Elevate (public site)

Direct selling & regulatory: Affiverse: MLM Regulatory Scrutiny & Affiliate Pivot 2025 (FTC 2024 report) · MLMinfopages: Beachbody/BODi Transition · Cosmetics Business: Rodan + Fields Model Revision · BeFormidable: Tupperware & the End of MLM Parties (incl. Modere closure)

MLM & network software: Infinite MLM: Top MLM Software Platforms USA (enterprise pricing $30K+) · Exigo (enterprise MLM software) · Rallyware: Direct Selling Software 2025

Agency & service pricing: Darkroom: Marketing Agency Cost 2026 · HawkSEM: Marketing Agency Pricing · Feedbird: Agency Pricing · Invesp: CRO Cost · ConversionRate.store: CRO Pricing · Flypost: Email Agency Cost · InfluencerFee: Influencer Agency Pricing · Favikon: Agency Charges · Track360: Outsourced Affiliate Management 2026 · Hamster Garage: Affiliate Management Services · Software Pricing Guide: Shopify Plus 2026 · Fractionus: Fractional CMO Cost · GoFractional: CMO Rates · Averi: CMO Cost Analysis

Software comparables: Eightx: True Cost of GRIN & impact.com · StackInfluence: Platform Pricing 2025 · Vendr: GRIN Contract Data · StackScored: GRIN Tiers · Omnisend: Klaviyo Pricing

Salary data: Glassdoor: Growth Marketing Manager NYC · Salary.com: Growth Marketing Manager SF · Salary.com: Marketing Director · Glassdoor: Marketing Director · Glassdoor: Content Marketing Manager · Glassdoor: Influencer Marketing Manager

Pricing psychology: SHNO: Pricing Psychology Statistics (anchoring, tier counts, Simon-Kucher ACV data) · Atticus: The Compromise Effect in Tier-Based Pricing · Evelance: Psychology Behind Pricing Tiers

Appendix A. Complete deliverable inventory (register v2)

Audit note. The source register (94 items) was decomposed from the Elevate One blueprint, an aspirational positioning document, and inherits three defects corrected here. Aspiration bias: Scout software and proof-engine tooling are product roadmap, not sellable deliverables; they are marked Roadmap and sold only as managed services. Overlaps: four items appear in two layers (UGC library in A3/A7; A/B testing in A2/A11; subscription journeys in A4/A8; storefront templates in A2/A6); each is cross-referenced to a single home. Omissions: the blueprint was written to sell a vision, not to run a client or a network; A12 adds twelve delivery-reality items evidenced by live contracts, and A13 adds five network-and-migration items from the public Elevate scope.

Where it lives: Strategy (Scope & Design) · Setup (Build & Launch) · Platform · MG (Managed Growth) · TK (Turnkey) · Bolt-on · Roadmap.

A1. Strategy & transition design (10 items → Strategy phase)

| Deliverable | Where it lives |

|---|---|

| Business model, product, customer & technology assessment | Strategy |

| Role design (customer, member, seller, creator, affiliate) | Strategy |

| Commercial, royalty & reward structure design (10+ tiers, tied to real sales) | Strategy |

| Offer architecture (product, subscription, membership) | Strategy |

| Lifecycle, social proof & retention design | Strategy |

| Creator programme, community journey & storefront model design | Strategy |

| Friends & Family and refer-a-friend rules design | Strategy |

| Content, claims, testimonial & UGC governance framework | Strategy |

| Pilot, migration & rollout roadmap (incl. market & regulatory scan) | Strategy |

| Measurement & reporting framework design | Strategy |

A2. Conversion commerce & personalisation (17 items → Setup builds; MG/TK operate)

| Deliverable | Where it lives |

|---|---|

| Full ecommerce website build | Setup |

| Product, collection & bundle pages | Setup |

| Campaign landing pages & advertorials | Setup (initial) → MG/TK ◐ (ongoing) |

| Seller/creator storefront templates | Setup → Platform (cross-ref: A6 storefronts) |

| Mobile-first checkout | Setup |

| One-time vs subscription comparison pages | Setup |

| Bundles, upsells, cross-sells, free-gift thresholds | Setup (build) → MG/TK (operate) |

| Multi-language / multi-market configuration | Setup → Platform |

| Headless commerce deployment | Bolt-on (scoped) |

| Product recommendation quizzes & guided finders | Setup (build) → MG/TK (operate) |

| Surveys & zero-party data capture | MG/TK |

| Multi-step lead forms & progressive profiling | Setup → MG/TK |

| Conditional funnel paths (answers, source, cart, behaviour) | MG/TK |

| Personalised bundles, subscriptions & offers | MG/TK |

| Popups, modals, sticky bars, exit-intent, cart recovery | Setup (build) → MG/TK (operate) |

| Source-specific pages (seller, creator, podcast, partner, paid, referral) | MG/TK ◐ |

| A/B testing & multi-step funnel analytics | MG ◐ 4/mo · TK ◐ 6/mo (single programme; cross-ref A11) |

A3. Social proof engine (7 items → capture free via missions; governance & deployment in TK)

| Deliverable | Where it lives |

|---|---|

| UGC & testimonial capture via missions | All tiers (missions engine) |

| Content rights, consent, disclosure & expiry tracking | TK (Roadmap: product tooling) |

| Review & testimonial approval workflows | TK; review-platform integration as Bolt-on |

| Tagged, searchable content & UGC library | TK (Roadmap) (single library; cross-ref A7) |

| Dynamic proof modules across the journey | TK |

| Proof A/B testing & proof-to-revenue reporting | TK |

| Winning-content loop (UGC into ads, email, storefronts) | TK |

A4. Recurring revenue (7 items → Setup builds; MG operates)

| Deliverable | Where it lives |

|---|---|

| Product subscriptions (subscribe & save, prepaid, frequency) | Setup (build) → MG (operate) |

| Pause / skip / swap controls & delivery notifications | Setup → MG |

| Failed-payment recovery & cancellation saves | MG |

| Subscription win-back campaigns | MG (journeys built in Setup; cross-ref A8) |

| Paid membership / Club programme (billing, tiers) | Setup (build) → MG (operate) |

| Member benefits, gifts & loyalty multipliers | MG |

| Membership renewal & upgrade journeys | MG |

A5. Customer advocacy (5 items → Platform infrastructure; MG activates)

| Deliverable | Where it lives |

|---|---|

| Refer-a-friend links, codes & fixed rewards | Platform |

| Double-sided referral rewards | Platform |

| Referral fraud controls, caps & approval delays | Platform |

| Friends & Family guest passes & shared benefits | Setup (config) → MG (operate) |

| Loyalty programme & member benefits | MG |

A6. Seller & creator commerce (7 items → Platform core)

| Deliverable | Where it lives |

|---|---|

| Personal seller/creator storefronts | Platform |

| Unique links, codes & offers | Platform |

| Campaigns & missions | Platform (infrastructure) · ops tiered |

| Royalty, commission, wallet & payout visibility | Platform |

| Claims, disclosure & content controls | Platform |

| Attribution across web, app & checkout | Platform |

| Creator video / review / UGC storefront modules | TK |

A7. Creator acquisition & operations / Scout (7 items → TK managed service today; Roadmap product)

| Deliverable | Where it lives |

|---|---|

| Creator discovery, search & qualification | TK managed service (Roadmap: Scout) |

| Personalised outreach & follow-up sequences | TK managed service (Roadmap: Scout) |

| Creator CRM: briefs, contracts, approvals, gifting, shipping | TK managed service (Roadmap: Scout) |

| UGC capture, rights & searchable library | TK (see A3; single library) |

| Affiliate code, storefront & sales performance tracking | Platform (live today) |

| Creator payments & commission approval | Platform (live today) |

| Creator, content & campaign reporting with recommendations | TK |

A8. Lifecycle automation (7 items → Setup builds flows; MG operates)

| Deliverable | Where it lives |

|---|---|

| Lead nurture & quiz-completion journeys | Setup → MG ◐ |

| Browse / cart / checkout recovery journeys | Setup → MG ◐ |

| Post-purchase, review-request & replenishment journeys | Setup → MG ◐ |

| Subscription onboarding, save & win-back journeys | Setup → MG ◐ (see A4) |

| Membership welcome, benefit & renewal journeys | Setup → MG ◐ |

| Referral prompt & reward-status journeys | Setup → MG ◐ |

| Seller/creator onboarding, activation & reactivation journeys | Setup → MG/TK ◐ |

A9. DTC content & demand engine (9 items → TK, with bolt-ons)

| Deliverable | Where it lives |

|---|---|

| Messaging architecture & creative strategy | Strategy (design) → TK (execution) |

| Creator seeding & UGC production calendar | TK |

| Customer testimonial & review programme | TK |

| Product & category education content | TK ◐ |

| Paid social & search creative variants | TK ◐ |

| Podcast, newsletter, partner & affiliate campaign pages | MG/TK ◐ (source-specific pages) |

| Giveaways, sampling, pop-ups & event activation | Bolt-on (TK ◐) |

| Email & newsletter content calendar | MG ◐ · TK ◐ |

| Regional, demographic & source-specific creative testing | TK ◐ / Bolt-on |

A10. LUUP platform infrastructure (10 items → Platform)

| Deliverable | Where it lives |

|---|---|

| Affiliate & referral tracking | Platform |

| Personal links, codes & storefronts | Platform |

| Missions & campaign management infrastructure | Platform |

| Royalties, rewards, commissions & wallet visibility | Platform |

| Approved content & compliance controls | Platform |

| Customer / member / seller / creator segmentation | Platform |

| Brand, region, language & role configuration | Platform |

| Enterprise reporting & attribution (disclosure-ready) | Platform |

| ERP / CRM / ecommerce / email / payment integrations | Bolt-on (scoped per client) |

| Global payouts via approved infrastructure | Platform |

A11. Managed growth & optimisation (8 items → tiered ownership)

| Deliverable | Where it lives |

|---|---|

| Launch planning & integrated campaign calendar | Setup → MG |

| Creator & field recruitment/activation operations | TK |

| CRO, A/B testing & funnel personalisation | MG ◐ · TK ◐ (see A2) |

| Lifecycle, subscription & membership campaign management | MG |

| Referral & membership activation campaigns | MG |

| Retention, churn & cohort analysis (customers & sellers) | TK (MBR) · MG Bolt-on |

| Weekly dashboards & monthly business reviews | TK (MG Bolt-on) |

| Quarterly growth roadmaps | TK |

A12. Delivery reality layer (12 items the blueprint never mentioned; sourced from live contracts and delivery)

| Deliverable | Where it lives | Evidence |

|---|---|---|

| Payment processor sourcing & high-risk merchant support | Bolt-on (from £5K) | Live contract includes it explicitly |

| Payout float management & reconciliation | Platform | Live contract float mechanics |

| KYC, tax documentation & self-billing for payout recipients | Platform | Required in every payout jurisdiction |

| Fraud, chargeback & attribution-integrity monitoring | Platform | GMV definition requires "net, verified" |

| Cookie consent, GDPR/CCPA operations & DPA management | Setup → Platform | Contract DPA obligations |

| Analytics & pixel implementation (GA4, server-side tagging, ad pixels) | Setup | Prerequisite for every attribution claim |

| Email/SMS deliverability (domains, warmup, list hygiene) | Setup → MG | Lifecycle revenue depends on it |

| 3PL / fulfilment integration & order-flow support | Setup | Live contract integration scope |

| Client team training & enablement | Setup (initial) · Bolt-on (ongoing) | Low adoption is the documented failure mode |

| Documentation & operational runbooks | Setup | Handover and audit requirement |

| Community / social channel management | Bolt-on | Frequently requested; never scoped in blueprint |

| Product photography & brand asset production | Bolt-on | Content engine needs source assets |

A13. Network & migration layer (5 items from the public Elevate scope; luup.com/elevate)

| Deliverable | Where it lives | Site reference |

|---|---|---|

| Native iOS + Android app build & store management | Setup (band 2–3) · Bolt-on from £25K | "Native apps available" |

| Royalty architecture modelling & configuration (10+ tiers) | Strategy (model) → Setup (configure) → Platform (run) | "Modelled with your team during design" |

| Field/seller data migration: records, network structure, earnings ledgers | Setup (migration band) | "Your data arrives whole" |

| Parallel-run payout reconciliation during transition | Setup (migration band) | "Payouts never skip a cycle" |

| Staged rollout by market/team with field training | Setup → Launch | "Rollout at your pace" |

Count check: 94 register items (A1–A11) + 12 delivery-reality items (A12) + 5 network & migration items (A13) = 111 mapped; 4 overlaps cross-referenced to single homes. Every item has exactly one commercial home; Roadmap items are sold only as managed services until the product ships.

Supporting artifacts: Elevate_One_Capability_Register.xlsx (source register; superseded by this Appendix pending its own v2 update) · Elevate_crossover_chart.png (Section 15).